28. 시계열 데이터#

import numpy as np

import pandas as pd

PREVIOUS_MAX_ROWS = pd.options.display.max_rows

pd.options.display.max_columns = 20

pd.options.display.max_rows = 20

pd.options.display.max_colwidth = 80

np.random.seed(12345)

np.set_printoptions(precision=4, suppress=True)

import matplotlib.pyplot as plt

plt.rc("figure", figsize=(10, 6))

28.1. datetime 자료형#

from datetime import datetime

now = datetime.now()

now

datetime.datetime(2023, 5, 26, 1, 21, 40, 533281)

print(now.year, now.month, now.day)

2023 5 26

delta = datetime(2011, 1, 7) - datetime(2009, 6, 24, 8, 15)

delta

datetime.timedelta(days=561, seconds=56700)

delta.days

561

delta.seconds

56700

from datetime import timedelta

start = datetime(2011, 1, 7)

start + timedelta(12)

datetime.datetime(2011, 1, 19, 0, 0)

start - 2 * timedelta(12)

datetime.datetime(2010, 12, 14, 0, 0)

28.1.1. 문자열과 Datetime#

stamp = datetime(2011, 1, 3)

str(stamp)

'2011-01-03 00:00:00'

stamp.strftime("%Y-%m-%d")

'2011-01-03'

value = "2011-01-03"

datetime.strptime(value, "%Y-%m-%d")

datetime.datetime(2011, 1, 3, 0, 0)

datestrs = ["7/6/2011", "8/6/2011"]

[datetime.strptime(x, "%m/%d/%Y") for x in datestrs]

[datetime.datetime(2011, 7, 6, 0, 0), datetime.datetime(2011, 8, 6, 0, 0)]

pd.to_datetime() 함수

datestrs = ["2011-07-06 12:00:00", "2011-08-06 00:00:00"]

pd.to_datetime(datestrs)

DatetimeIndex(['2011-07-06 12:00:00', '2011-08-06 00:00:00'], dtype='datetime64[ns]', freq=None)

idx = pd.to_datetime(datestrs + [None])

idx

DatetimeIndex(['2011-07-06 12:00:00', '2011-08-06 00:00:00', 'NaT'], dtype='datetime64[ns]', freq=None)

idx[2]

NaT

pd.isna(idx)

array([False, False, True])

28.2. 시계열 데이터 기초#

dates = [datetime(2011, 1, 2), datetime(2011, 1, 5),

datetime(2011, 1, 7), datetime(2011, 1, 8),

datetime(2011, 1, 10), datetime(2011, 1, 12)]

ts = pd.Series(np.random.standard_normal(6), index=dates)

ts

2011-01-02 -0.204708

2011-01-05 0.478943

2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

2011-01-12 1.393406

dtype: float64

ts.index

DatetimeIndex(['2011-01-02', '2011-01-05', '2011-01-07', '2011-01-08',

'2011-01-10', '2011-01-12'],

dtype='datetime64[ns]', freq=None)

ts + ts[::2]

2011-01-02 -0.409415

2011-01-05 NaN

2011-01-07 -1.038877

2011-01-08 NaN

2011-01-10 3.931561

2011-01-12 NaN

dtype: float64

ts.index

DatetimeIndex(['2011-01-02', '2011-01-05', '2011-01-07', '2011-01-08',

'2011-01-10', '2011-01-12'],

dtype='datetime64[ns]', freq=None)

ts.index.dtype

dtype('<M8[ns]')

stamp = ts.index[0]

stamp

Timestamp('2011-01-02 00:00:00')

28.2.1. 인덱싱, 선택, 슬라이싱#

stamp = ts.index[2]

ts[stamp]

-0.5194387150567381

ts["2011-01-10"]

1.9657805725027142

longer_ts = pd.Series(np.random.standard_normal(1000),

index=pd.date_range("2000-01-01", periods=1000))

longer_ts

2000-01-01 0.092908

2000-01-02 0.281746

2000-01-03 0.769023

2000-01-04 1.246435

2000-01-05 1.007189

...

2002-09-22 0.930944

2002-09-23 -0.811676

2002-09-24 -1.830156

2002-09-25 -0.138730

2002-09-26 0.334088

Freq: D, Length: 1000, dtype: float64

longer_ts["2001"]

2001-01-01 1.599534

2001-01-02 0.474071

2001-01-03 0.151326

2001-01-04 -0.542173

2001-01-05 -0.475496

...

2001-12-27 0.057874

2001-12-28 -0.433739

2001-12-29 0.092698

2001-12-30 -1.397820

2001-12-31 1.457823

Freq: D, Length: 365, dtype: float64

longer_ts["2001-05"]

2001-05-01 -0.622547

2001-05-02 0.936289

2001-05-03 0.750018

2001-05-04 -0.056715

2001-05-05 2.300675

...

2001-05-27 0.235477

2001-05-28 0.111835

2001-05-29 -1.251504

2001-05-30 -2.949343

2001-05-31 0.634634

Freq: D, Length: 31, dtype: float64

ts[datetime(2011, 1, 7):]

2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

2011-01-12 1.393406

dtype: float64

ts[datetime(2011, 1, 7):datetime(2011, 1, 10)]

2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

dtype: float64

ts

2011-01-02 -0.204708

2011-01-05 0.478943

2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

2011-01-12 1.393406

dtype: float64

ts["2011-01-06":"2011-01-11"]

2011-01-07 -0.519439

2011-01-08 -0.555730

2011-01-10 1.965781

dtype: float64

ts.truncate(after="2011-01-09")

2011-01-02 -0.204708

2011-01-05 0.478943

2011-01-07 -0.519439

2011-01-08 -0.555730

dtype: float64

dates = pd.date_range("2000-01-01", periods=100, freq="W-WED")

long_df = pd.DataFrame(np.random.standard_normal((100, 4)),

index=dates,

columns=["Colorado", "Texas", "New York", "Ohio"])

long_df

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | 0.488675 | -0.178098 | 2.122315 | 0.061192 |

| 2000-01-12 | 0.884111 | -0.608506 | -0.072052 | 0.544066 |

| 2000-01-19 | 0.323886 | -1.683325 | 0.526860 | 1.858791 |

| 2000-01-26 | -0.548419 | -0.279397 | -0.021299 | -0.287990 |

| 2000-02-02 | 0.089175 | 0.522858 | 0.572796 | -1.760372 |

| ... | ... | ... | ... | ... |

| 2001-10-31 | -0.054630 | -0.656506 | -1.550087 | -0.044347 |

| 2001-11-07 | 0.681470 | -0.953726 | -1.857016 | 0.449495 |

| 2001-11-14 | -0.061732 | 1.233914 | 0.705830 | -1.309077 |

| 2001-11-21 | -1.537380 | 0.531551 | 2.047573 | 0.446691 |

| 2001-11-28 | -0.223556 | 0.092835 | 0.716076 | 0.657198 |

100 rows × 4 columns

long_df.loc["2001-05"]

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2001-05-02 | -0.006045 | 0.490094 | -0.277186 | -0.707213 |

| 2001-05-09 | -0.560107 | 2.735527 | 0.927335 | 1.513906 |

| 2001-05-16 | 0.538600 | 1.273768 | 0.667876 | -0.969206 |

| 2001-05-23 | 1.676091 | -0.817649 | 0.050188 | 1.951312 |

| 2001-05-30 | 3.260383 | 0.963301 | 1.201206 | -1.852001 |

28.2.2. 중복 인덱스 라벨을 갖는 시계열 데이터#

dates = pd.DatetimeIndex(["2000-01-01", "2000-01-02", "2000-01-02",

"2000-01-02", "2000-01-03"])

dup_ts = pd.Series(np.arange(5), index=dates)

dup_ts

2000-01-01 0

2000-01-02 1

2000-01-02 2

2000-01-02 3

2000-01-03 4

dtype: int32

dup_ts.index.is_unique

False

dup_ts["2000-01-03"] # not duplicated

4

dup_ts["2000-01-02"] # duplicated

2000-01-02 1

2000-01-02 2

2000-01-02 3

dtype: int32

grouped = dup_ts.groupby(level=0)

grouped.mean()

2000-01-01 0.0

2000-01-02 2.0

2000-01-03 4.0

dtype: float64

grouped.count()

2000-01-01 1

2000-01-02 3

2000-01-03 1

dtype: int64

28.3. 날짜 구간 인덱스, 빈도, 시프팅#

28.3.1. 날짜 구간 인덱스 생성#

index = pd.date_range("2012-04-01", "2012-06-01")

index

DatetimeIndex(['2012-04-01', '2012-04-02', '2012-04-03', '2012-04-04',

'2012-04-05', '2012-04-06', '2012-04-07', '2012-04-08',

'2012-04-09', '2012-04-10', '2012-04-11', '2012-04-12',

'2012-04-13', '2012-04-14', '2012-04-15', '2012-04-16',

'2012-04-17', '2012-04-18', '2012-04-19', '2012-04-20',

'2012-04-21', '2012-04-22', '2012-04-23', '2012-04-24',

'2012-04-25', '2012-04-26', '2012-04-27', '2012-04-28',

'2012-04-29', '2012-04-30', '2012-05-01', '2012-05-02',

'2012-05-03', '2012-05-04', '2012-05-05', '2012-05-06',

'2012-05-07', '2012-05-08', '2012-05-09', '2012-05-10',

'2012-05-11', '2012-05-12', '2012-05-13', '2012-05-14',

'2012-05-15', '2012-05-16', '2012-05-17', '2012-05-18',

'2012-05-19', '2012-05-20', '2012-05-21', '2012-05-22',

'2012-05-23', '2012-05-24', '2012-05-25', '2012-05-26',

'2012-05-27', '2012-05-28', '2012-05-29', '2012-05-30',

'2012-05-31', '2012-06-01'],

dtype='datetime64[ns]', freq='D')

pd.date_range(start="2012-04-01", periods=20)

DatetimeIndex(['2012-04-01', '2012-04-02', '2012-04-03', '2012-04-04',

'2012-04-05', '2012-04-06', '2012-04-07', '2012-04-08',

'2012-04-09', '2012-04-10', '2012-04-11', '2012-04-12',

'2012-04-13', '2012-04-14', '2012-04-15', '2012-04-16',

'2012-04-17', '2012-04-18', '2012-04-19', '2012-04-20'],

dtype='datetime64[ns]', freq='D')

pd.date_range(end="2012-06-01", periods=20)

DatetimeIndex(['2012-05-13', '2012-05-14', '2012-05-15', '2012-05-16',

'2012-05-17', '2012-05-18', '2012-05-19', '2012-05-20',

'2012-05-21', '2012-05-22', '2012-05-23', '2012-05-24',

'2012-05-25', '2012-05-26', '2012-05-27', '2012-05-28',

'2012-05-29', '2012-05-30', '2012-05-31', '2012-06-01'],

dtype='datetime64[ns]', freq='D')

pd.date_range("2000-01-01", "2000-12-01", freq="BM")

DatetimeIndex(['2000-01-31', '2000-02-29', '2000-03-31', '2000-04-28',

'2000-05-31', '2000-06-30', '2000-07-31', '2000-08-31',

'2000-09-29', '2000-10-31', '2000-11-30'],

dtype='datetime64[ns]', freq='BM')

pd.date_range("2012-05-02 12:56:31", periods=5)

DatetimeIndex(['2012-05-02 12:56:31', '2012-05-03 12:56:31',

'2012-05-04 12:56:31', '2012-05-05 12:56:31',

'2012-05-06 12:56:31'],

dtype='datetime64[ns]', freq='D')

pd.date_range("2012-05-02 12:56:31", periods=5, normalize=True)

DatetimeIndex(['2012-05-02', '2012-05-03', '2012-05-04', '2012-05-05',

'2012-05-06'],

dtype='datetime64[ns]', freq='D')

28.3.2. 빈도와 빈도 단위#

from pandas.tseries.offsets import Hour, Minute

hour = Hour()

hour

<Hour>

four_hours = Hour(4)

four_hours

<4 * Hours>

pd.date_range("2000-01-01", "2000-01-03 23:59", freq="4H")

DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 04:00:00',

'2000-01-01 08:00:00', '2000-01-01 12:00:00',

'2000-01-01 16:00:00', '2000-01-01 20:00:00',

'2000-01-02 00:00:00', '2000-01-02 04:00:00',

'2000-01-02 08:00:00', '2000-01-02 12:00:00',

'2000-01-02 16:00:00', '2000-01-02 20:00:00',

'2000-01-03 00:00:00', '2000-01-03 04:00:00',

'2000-01-03 08:00:00', '2000-01-03 12:00:00',

'2000-01-03 16:00:00', '2000-01-03 20:00:00'],

dtype='datetime64[ns]', freq='4H')

Hour(2) + Minute(30)

<150 * Minutes>

pd.date_range("2000-01-01", periods=10, freq="1h30min")

DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 01:30:00',

'2000-01-01 03:00:00', '2000-01-01 04:30:00',

'2000-01-01 06:00:00', '2000-01-01 07:30:00',

'2000-01-01 09:00:00', '2000-01-01 10:30:00',

'2000-01-01 12:00:00', '2000-01-01 13:30:00'],

dtype='datetime64[ns]', freq='90T')

monthly_dates = pd.date_range("2012-01-01", "2012-09-01", freq="WOM-3FRI")

list(monthly_dates)

[Timestamp('2012-01-20 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-02-17 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-03-16 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-04-20 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-05-18 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-06-15 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-07-20 00:00:00', freq='WOM-3FRI'),

Timestamp('2012-08-17 00:00:00', freq='WOM-3FRI')]

28.3.3. 데이터 시프팅#

ts = pd.Series(np.random.standard_normal(4),

index=pd.date_range("2000-01-01", periods=4, freq="M"))

ts

2000-01-31 -0.066748

2000-02-29 0.838639

2000-03-31 -0.117388

2000-04-30 -0.517795

Freq: M, dtype: float64

ts.shift(2)

2000-01-31 NaN

2000-02-29 NaN

2000-03-31 -0.066748

2000-04-30 0.838639

Freq: M, dtype: float64

ts.shift(-2)

2000-01-31 -0.117388

2000-02-29 -0.517795

2000-03-31 NaN

2000-04-30 NaN

Freq: M, dtype: float64

ts.shift(2, freq="M")

2000-03-31 -0.066748

2000-04-30 0.838639

2000-05-31 -0.117388

2000-06-30 -0.517795

Freq: M, dtype: float64

ts.shift(3, freq="D")

2000-02-03 -0.066748

2000-03-03 0.838639

2000-04-03 -0.117388

2000-05-03 -0.517795

dtype: float64

ts.shift(1, freq="90T")

2000-01-31 01:30:00 -0.066748

2000-02-29 01:30:00 0.838639

2000-03-31 01:30:00 -0.117388

2000-04-30 01:30:00 -0.517795

dtype: float64

offset 활용 시프팅

from pandas.tseries.offsets import Day, MonthEnd

now = datetime(2011, 11, 17)

now + 3 * Day()

Timestamp('2011-11-20 00:00:00')

now + MonthEnd()

Timestamp('2011-11-30 00:00:00')

now + MonthEnd(2)

Timestamp('2011-12-31 00:00:00')

offset = MonthEnd()

offset.rollforward(now)

Timestamp('2011-11-30 00:00:00')

offset.rollback(now)

Timestamp('2011-10-31 00:00:00')

ts = pd.Series(np.random.standard_normal(20),

index=pd.date_range("2000-01-15", periods=20, freq="4D"))

ts

2000-01-15 -0.116696

2000-01-19 2.389645

2000-01-23 -0.932454

2000-01-27 -0.229331

2000-01-31 -1.140330

2000-02-04 0.439920

2000-02-08 -0.823758

2000-02-12 -0.520930

2000-02-16 0.350282

2000-02-20 0.204395

2000-02-24 0.133445

2000-02-28 0.327905

2000-03-03 0.072153

2000-03-07 0.131678

2000-03-11 -1.297459

2000-03-15 0.997747

2000-03-19 0.870955

2000-03-23 -0.991253

2000-03-27 0.151699

2000-03-31 1.266151

Freq: 4D, dtype: float64

ts.groupby(MonthEnd().rollforward).mean()

2000-01-31 -0.005833

2000-02-29 0.015894

2000-03-31 0.150209

dtype: float64

ts.resample("M").mean()

2000-01-31 -0.005833

2000-02-29 0.015894

2000-03-31 0.150209

Freq: M, dtype: float64

28.4. 시간대#

import pytz

pytz.common_timezones[-5:]

['US/Eastern', 'US/Hawaii', 'US/Mountain', 'US/Pacific', 'UTC']

tz = pytz.timezone("America/New_York")

tz

<DstTzInfo 'America/New_York' LMT-1 day, 19:04:00 STD>

28.4.1. 시간대 지정#

dates = pd.date_range("2012-03-09 09:30", periods=6)

ts = pd.Series(np.random.standard_normal(len(dates)), index=dates)

ts

2012-03-09 09:30:00 -0.202469

2012-03-10 09:30:00 0.050718

2012-03-11 09:30:00 0.639869

2012-03-12 09:30:00 0.597594

2012-03-13 09:30:00 -0.797246

2012-03-14 09:30:00 0.472879

Freq: D, dtype: float64

print(ts.index.tz)

None

pd.date_range("2012-03-09 09:30", periods=10, tz="UTC")

DatetimeIndex(['2012-03-09 09:30:00+00:00', '2012-03-10 09:30:00+00:00',

'2012-03-11 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00',

'2012-03-15 09:30:00+00:00', '2012-03-16 09:30:00+00:00',

'2012-03-17 09:30:00+00:00', '2012-03-18 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')

ts

2012-03-09 09:30:00 -0.202469

2012-03-10 09:30:00 0.050718

2012-03-11 09:30:00 0.639869

2012-03-12 09:30:00 0.597594

2012-03-13 09:30:00 -0.797246

2012-03-14 09:30:00 0.472879

Freq: D, dtype: float64

ts_utc = ts.tz_localize("UTC")

ts_utc

2012-03-09 09:30:00+00:00 -0.202469

2012-03-10 09:30:00+00:00 0.050718

2012-03-11 09:30:00+00:00 0.639869

2012-03-12 09:30:00+00:00 0.597594

2012-03-13 09:30:00+00:00 -0.797246

2012-03-14 09:30:00+00:00 0.472879

Freq: D, dtype: float64

ts_utc.index

DatetimeIndex(['2012-03-09 09:30:00+00:00', '2012-03-10 09:30:00+00:00',

'2012-03-11 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')

ts_utc.tz_convert("America/New_York")

2012-03-09 04:30:00-05:00 -0.202469

2012-03-10 04:30:00-05:00 0.050718

2012-03-11 05:30:00-04:00 0.639869

2012-03-12 05:30:00-04:00 0.597594

2012-03-13 05:30:00-04:00 -0.797246

2012-03-14 05:30:00-04:00 0.472879

Freq: D, dtype: float64

ts_eastern = ts.tz_localize("America/New_York")

ts_eastern.tz_convert("UTC")

2012-03-09 14:30:00+00:00 -0.202469

2012-03-10 14:30:00+00:00 0.050718

2012-03-11 13:30:00+00:00 0.639869

2012-03-12 13:30:00+00:00 0.597594

2012-03-13 13:30:00+00:00 -0.797246

2012-03-14 13:30:00+00:00 0.472879

dtype: float64

ts_eastern.tz_convert("Europe/Berlin")

2012-03-09 15:30:00+01:00 -0.202469

2012-03-10 15:30:00+01:00 0.050718

2012-03-11 14:30:00+01:00 0.639869

2012-03-12 14:30:00+01:00 0.597594

2012-03-13 14:30:00+01:00 -0.797246

2012-03-14 14:30:00+01:00 0.472879

dtype: float64

ts.index.tz_localize("Asia/Shanghai")

DatetimeIndex(['2012-03-09 09:30:00+08:00', '2012-03-10 09:30:00+08:00',

'2012-03-11 09:30:00+08:00', '2012-03-12 09:30:00+08:00',

'2012-03-13 09:30:00+08:00', '2012-03-14 09:30:00+08:00'],

dtype='datetime64[ns, Asia/Shanghai]', freq=None)

28.4.2. 시간대와 타임 스탬프#

stamp = pd.Timestamp("2011-03-12 04:00")

stamp_utc = stamp.tz_localize("utc")

stamp_utc.tz_convert("America/New_York")

Timestamp('2011-03-11 23:00:00-0500', tz='America/New_York')

stamp_moscow = pd.Timestamp("2011-03-12 04:00", tz="Europe/Moscow")

stamp_moscow

Timestamp('2011-03-12 04:00:00+0300', tz='Europe/Moscow')

stamp_utc.value

1299902400000000000

stamp_utc.tz_convert("America/New_York").value

1299902400000000000

stamp = pd.Timestamp("2012-03-11 01:30", tz="US/Eastern")

stamp

Timestamp('2012-03-11 01:30:00-0500', tz='US/Eastern')

stamp + Hour()

Timestamp('2012-03-11 03:30:00-0400', tz='US/Eastern')

stamp = pd.Timestamp("2012-11-04 00:30", tz="US/Eastern")

stamp

Timestamp('2012-11-04 00:30:00-0400', tz='US/Eastern')

stamp + 2 * Hour()

Timestamp('2012-11-04 01:30:00-0500', tz='US/Eastern')

28.4.3. 다른 시간대 다루기#

dates = pd.date_range("2012-03-07 09:30", periods=10, freq="B")

ts = pd.Series(np.random.standard_normal(len(dates)), index=dates)

ts

2012-03-07 09:30:00 0.522356

2012-03-08 09:30:00 -0.546348

2012-03-09 09:30:00 -0.733537

2012-03-12 09:30:00 1.302736

2012-03-13 09:30:00 0.022199

2012-03-14 09:30:00 0.364287

2012-03-15 09:30:00 -0.922839

2012-03-16 09:30:00 0.312656

2012-03-19 09:30:00 -1.128497

2012-03-20 09:30:00 -0.333488

Freq: B, dtype: float64

ts1 = ts[:7].tz_localize("Europe/London")

ts2 = ts1[2:].tz_convert("Europe/Moscow")

result = ts1 + ts2

result.index

DatetimeIndex(['2012-03-07 09:30:00+00:00', '2012-03-08 09:30:00+00:00',

'2012-03-09 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00',

'2012-03-15 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq=None)

28.5. 기간 연산#

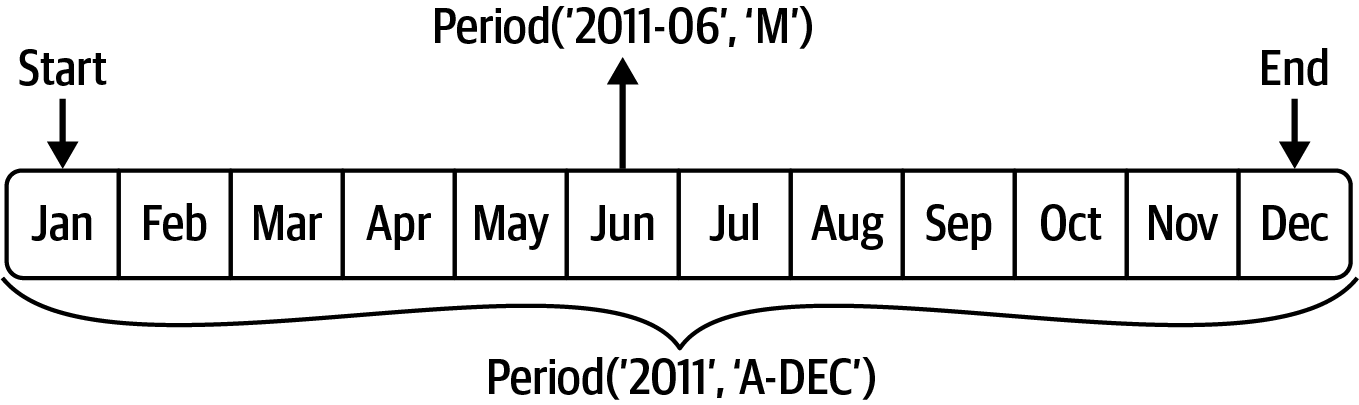

p = pd.Period("2011", freq="A-DEC")

p

Period('2011', 'A-DEC')

p + 5

Period('2016', 'A-DEC')

p - 2

Period('2009', 'A-DEC')

pd.Period("2014", freq="A-DEC") - p

<3 * YearEnds: month=12>

periods = pd.period_range("2000-01-01", "2000-06-30", freq="M")

periods

PeriodIndex(['2000-01', '2000-02', '2000-03', '2000-04', '2000-05', '2000-06'], dtype='period[M]')

pd.Series(np.random.standard_normal(6), index=periods)

2000-01 -0.514551

2000-02 -0.559782

2000-03 -0.783408

2000-04 -1.797685

2000-05 -0.172670

2000-06 0.680215

Freq: M, dtype: float64

values = ["2001Q3", "2002Q2", "2003Q1"]

index = pd.PeriodIndex(values, freq="Q-DEC")

index

PeriodIndex(['2001Q3', '2002Q2', '2003Q1'], dtype='period[Q-DEC]')

28.5.1. 기간 빈도 변환#

p = pd.Period("2011", freq="A-DEC")

p

Period('2011', 'A-DEC')

p.asfreq("M", how="start")

Period('2011-01', 'M')

p.asfreq("M", how="end")

Period('2011-12', 'M')

p.asfreq("M")

Period('2011-12', 'M')

p = pd.Period("2011", freq="A-JUN")

p

Period('2011', 'A-JUN')

p.asfreq("M", how="start")

Period('2010-07', 'M')

p.asfreq("M", how="end")

Period('2011-06', 'M')

<그림 출처: Python for Data Analysis>

p = pd.Period("Aug-2011", "M")

p.asfreq("A-JUN")

Period('2012', 'A-JUN')

periods = pd.period_range("2006", "2009", freq="A-DEC")

ts = pd.Series(np.random.standard_normal(len(periods)), index=periods)

ts

2006 1.607578

2007 0.200381

2008 -0.834068

2009 -0.302988

Freq: A-DEC, dtype: float64

ts.asfreq("M", how="start")

2006-01 1.607578

2007-01 0.200381

2008-01 -0.834068

2009-01 -0.302988

Freq: M, dtype: float64

ts.asfreq("B", how="end")

2006-12-29 1.607578

2007-12-31 0.200381

2008-12-31 -0.834068

2009-12-31 -0.302988

Freq: B, dtype: float64

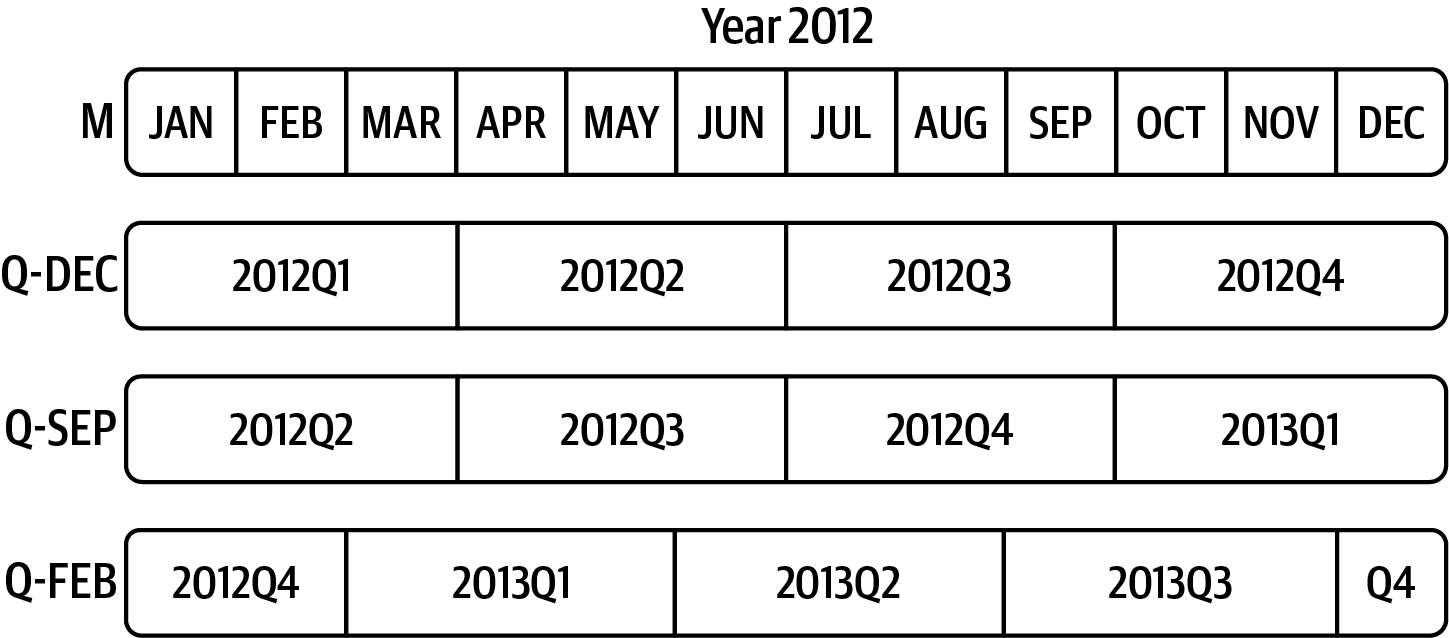

28.5.2. 분기 단위 기간#

p = pd.Period("2012Q4", freq="Q-JAN")

p

Period('2012Q4', 'Q-JAN')

p.asfreq("D", how="start")

Period('2011-11-01', 'D')

p.asfreq("D", how="end")

Period('2012-01-31', 'D')

<그림 출처: Python for Data Analysis>

p4pm = (p.asfreq("B", how="end") - 1).asfreq("T", how="start") + 16 * 60

p4pm

Period('2012-01-30 16:00', 'T')

p4pm.to_timestamp()

Timestamp('2012-01-30 16:00:00')

periods = pd.period_range("2011Q3", "2012Q4", freq="Q-JAN")

ts = pd.Series(np.arange(len(periods)), index=periods)

ts

2011Q3 0

2011Q4 1

2012Q1 2

2012Q2 3

2012Q3 4

2012Q4 5

Freq: Q-JAN, dtype: int32

new_periods = (periods.asfreq("B", "end") - 1).asfreq("H", "start") + 16

ts.index = new_periods.to_timestamp()

ts

2010-10-28 16:00:00 0

2011-01-28 16:00:00 1

2011-04-28 16:00:00 2

2011-07-28 16:00:00 3

2011-10-28 16:00:00 4

2012-01-30 16:00:00 5

dtype: int32

28.5.3. 타임 스탬프와 기간#

dates = pd.date_range("2000-01-01", periods=3, freq="M")

ts = pd.Series(np.random.standard_normal(3), index=dates)

ts

2000-01-31 1.663261

2000-02-29 -0.996206

2000-03-31 1.521760

Freq: M, dtype: float64

pts = ts.to_period()

pts

2000-01 1.663261

2000-02 -0.996206

2000-03 1.521760

Freq: M, dtype: float64

dates = pd.date_range("2000-01-29", periods=6)

ts2 = pd.Series(np.random.standard_normal(6), index=dates)

ts2

2000-01-29 0.244175

2000-01-30 0.423331

2000-01-31 -0.654040

2000-02-01 2.089154

2000-02-02 -0.060220

2000-02-03 -0.167933

Freq: D, dtype: float64

ts2.to_period("M")

2000-01 0.244175

2000-01 0.423331

2000-01 -0.654040

2000-02 2.089154

2000-02 -0.060220

2000-02 -0.167933

Freq: M, dtype: float64

pts = ts2.to_period()

pts

2000-01-29 0.244175

2000-01-30 0.423331

2000-01-31 -0.654040

2000-02-01 2.089154

2000-02-02 -0.060220

2000-02-03 -0.167933

Freq: D, dtype: float64

pts.to_timestamp(how="end")

2000-01-29 23:59:59.999999999 0.244175

2000-01-30 23:59:59.999999999 0.423331

2000-01-31 23:59:59.999999999 -0.654040

2000-02-01 23:59:59.999999999 2.089154

2000-02-02 23:59:59.999999999 -0.060220

2000-02-03 23:59:59.999999999 -0.167933

Freq: D, dtype: float64

28.5.4. 기간 인덱스#

base_url = "https://raw.githubusercontent.com/codingalzi/datapy/master/jupyter-book/examples/"

file = "macrodata.csv"

data = pd.read_csv(base_url+file)

data.head(5)

| year | quarter | realgdp | realcons | realinv | realgovt | realdpi | cpi | m1 | tbilrate | unemp | pop | infl | realint | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1959.0 | 1.0 | 2710.349 | 1707.4 | 286.898 | 470.045 | 1886.9 | 28.98 | 139.7 | 2.82 | 5.8 | 177.146 | 0.00 | 0.00 |

| 1 | 1959.0 | 2.0 | 2778.801 | 1733.7 | 310.859 | 481.301 | 1919.7 | 29.15 | 141.7 | 3.08 | 5.1 | 177.830 | 2.34 | 0.74 |

| 2 | 1959.0 | 3.0 | 2775.488 | 1751.8 | 289.226 | 491.260 | 1916.4 | 29.35 | 140.5 | 3.82 | 5.3 | 178.657 | 2.74 | 1.09 |

| 3 | 1959.0 | 4.0 | 2785.204 | 1753.7 | 299.356 | 484.052 | 1931.3 | 29.37 | 140.0 | 4.33 | 5.6 | 179.386 | 0.27 | 4.06 |

| 4 | 1960.0 | 1.0 | 2847.699 | 1770.5 | 331.722 | 462.199 | 1955.5 | 29.54 | 139.6 | 3.50 | 5.2 | 180.007 | 2.31 | 1.19 |

data["year"]

0 1959.0

1 1959.0

2 1959.0

3 1959.0

4 1960.0

...

198 2008.0

199 2008.0

200 2009.0

201 2009.0

202 2009.0

Name: year, Length: 203, dtype: float64

data["quarter"]

0 1.0

1 2.0

2 3.0

3 4.0

4 1.0

...

198 3.0

199 4.0

200 1.0

201 2.0

202 3.0

Name: quarter, Length: 203, dtype: float64

index = pd.PeriodIndex(year=data["year"], quarter=data["quarter"],

freq="Q-DEC")

index

PeriodIndex(['1959Q1', '1959Q2', '1959Q3', '1959Q4', '1960Q1', '1960Q2',

'1960Q3', '1960Q4', '1961Q1', '1961Q2',

...

'2007Q2', '2007Q3', '2007Q4', '2008Q1', '2008Q2', '2008Q3',

'2008Q4', '2009Q1', '2009Q2', '2009Q3'],

dtype='period[Q-DEC]', length=203)

data.index = index

data["infl"]

1959Q1 0.00

1959Q2 2.34

1959Q3 2.74

1959Q4 0.27

1960Q1 2.31

...

2008Q3 -3.16

2008Q4 -8.79

2009Q1 0.94

2009Q2 3.37

2009Q3 3.56

Freq: Q-DEC, Name: infl, Length: 203, dtype: float64

28.6. 리샘플링#

dates = pd.date_range("2000-01-01", periods=100)

ts = pd.Series(np.random.standard_normal(len(dates)), index=dates)

ts

2000-01-01 0.631634

2000-01-02 -1.594313

2000-01-03 -1.519937

2000-01-04 1.108752

2000-01-05 1.255853

...

2000-04-05 -0.423776

2000-04-06 0.789740

2000-04-07 0.937568

2000-04-08 -2.253294

2000-04-09 -1.772919

Freq: D, Length: 100, dtype: float64

ts.resample("M").mean()

2000-01-31 -0.165893

2000-02-29 0.078606

2000-03-31 0.223811

2000-04-30 -0.063643

Freq: M, dtype: float64

ts.resample("M", kind="period").mean()

2000-01 -0.165893

2000-02 0.078606

2000-03 0.223811

2000-04 -0.063643

Freq: M, dtype: float64

28.6.1. 다운 샘플링#

dates = pd.date_range("2000-01-01", periods=12, freq="T")

ts = pd.Series(np.arange(len(dates)), index=dates)

ts

2000-01-01 00:00:00 0

2000-01-01 00:01:00 1

2000-01-01 00:02:00 2

2000-01-01 00:03:00 3

2000-01-01 00:04:00 4

2000-01-01 00:05:00 5

2000-01-01 00:06:00 6

2000-01-01 00:07:00 7

2000-01-01 00:08:00 8

2000-01-01 00:09:00 9

2000-01-01 00:10:00 10

2000-01-01 00:11:00 11

Freq: T, dtype: int32

ts.resample("5min").sum()

2000-01-01 00:00:00 10

2000-01-01 00:05:00 35

2000-01-01 00:10:00 21

Freq: 5T, dtype: int32

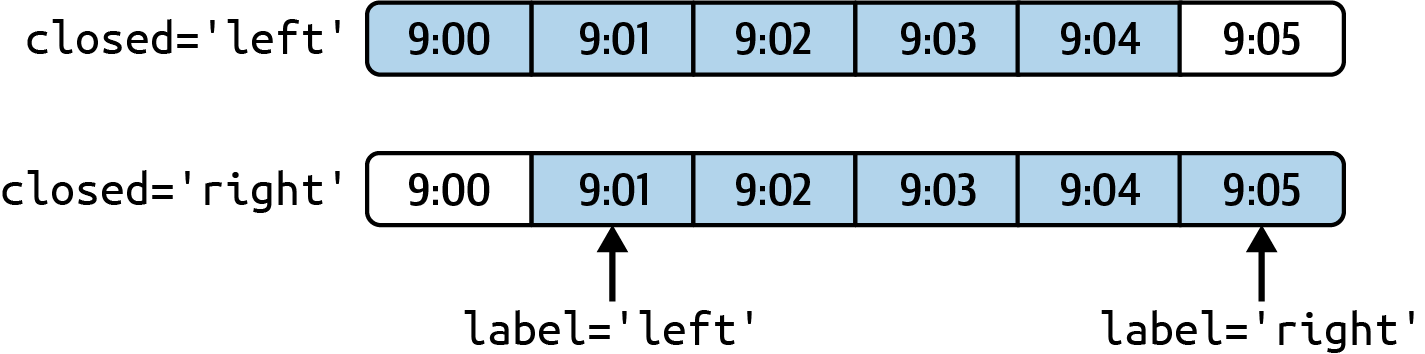

ts.resample("5min", closed="right").sum()

1999-12-31 23:55:00 0

2000-01-01 00:00:00 15

2000-01-01 00:05:00 40

2000-01-01 00:10:00 11

Freq: 5T, dtype: int32

ts.resample("5min", closed="right", label="right").sum()

2000-01-01 00:00:00 0

2000-01-01 00:05:00 15

2000-01-01 00:10:00 40

2000-01-01 00:15:00 11

Freq: 5T, dtype: int32

<그림 출처: Python for Data Analysis>

from pandas.tseries.frequencies import to_offset

result = ts.resample("5min", closed="right", label="right").sum()

result.index = result.index + to_offset("-1s")

result

1999-12-31 23:59:59 0

2000-01-01 00:04:59 15

2000-01-01 00:09:59 40

2000-01-01 00:14:59 11

Freq: 5T, dtype: int32

ts = pd.Series(np.random.permutation(np.arange(len(dates))), index=dates)

ts.resample("5min").ohlc()

| open | high | low | close | |

|---|---|---|---|---|

| 2000-01-01 00:00:00 | 8 | 8 | 1 | 5 |

| 2000-01-01 00:05:00 | 6 | 11 | 2 | 2 |

| 2000-01-01 00:10:00 | 0 | 7 | 0 | 7 |

28.6.2. 업샘플링과 보간법#

frame = pd.DataFrame(np.random.standard_normal((2, 4)),

index=pd.date_range("2000-01-01", periods=2,

freq="W-WED"),

columns=["Colorado", "Texas", "New York", "Ohio"])

frame

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-12 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

df_daily = frame.resample("D").asfreq()

df_daily

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-06 | NaN | NaN | NaN | NaN |

| 2000-01-07 | NaN | NaN | NaN | NaN |

| 2000-01-08 | NaN | NaN | NaN | NaN |

| 2000-01-09 | NaN | NaN | NaN | NaN |

| 2000-01-10 | NaN | NaN | NaN | NaN |

| 2000-01-11 | NaN | NaN | NaN | NaN |

| 2000-01-12 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

frame.resample("D").ffill()

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-06 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-07 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-08 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-09 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-10 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-11 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-12 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

frame.resample("D").ffill(limit=2)

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-05 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-06 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-07 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-08 | NaN | NaN | NaN | NaN |

| 2000-01-09 | NaN | NaN | NaN | NaN |

| 2000-01-10 | NaN | NaN | NaN | NaN |

| 2000-01-11 | NaN | NaN | NaN | NaN |

| 2000-01-12 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

frame.resample("W-THU").ffill()

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01-06 | -0.896431 | 0.927238 | 0.482284 | -0.867130 |

| 2000-01-13 | 0.493841 | -0.155434 | 1.397286 | 1.507055 |

28.6.3. 기간 활용 리샘플링#

frame = pd.DataFrame(np.random.standard_normal((24, 4)),

index=pd.period_range("1-2000", "12-2001",

freq="M"),

columns=["Colorado", "Texas", "New York", "Ohio"])

frame.head()

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000-01 | -1.179442 | 0.443171 | 1.395676 | -0.529658 |

| 2000-02 | 0.787358 | 0.248845 | 0.743239 | 1.267746 |

| 2000-03 | 1.302395 | -0.272154 | -0.051532 | -0.467740 |

| 2000-04 | -1.040816 | 0.426419 | 0.312945 | -1.115689 |

| 2000-05 | 1.234297 | -1.893094 | -1.661605 | -0.005477 |

annual_frame = frame.resample("A-DEC").mean()

annual_frame

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

# Q-DEC: Quarterly, year ending in December

annual_frame.resample("Q-DEC").ffill()

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000Q1 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2000Q2 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2000Q3 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2000Q4 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q1 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2001Q2 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2001Q3 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2001Q4 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

annual_frame.resample("Q-DEC", convention="end").asfreq()

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000Q4 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q1 | NaN | NaN | NaN | NaN |

| 2001Q2 | NaN | NaN | NaN | NaN |

| 2001Q3 | NaN | NaN | NaN | NaN |

| 2001Q4 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

annual_frame.resample("Q-MAR").ffill()

| Colorado | Texas | New York | Ohio | |

|---|---|---|---|---|

| 2000Q4 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q1 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q2 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q3 | 0.487329 | 0.104466 | 0.020495 | -0.273945 |

| 2001Q4 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2002Q1 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2002Q2 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

| 2002Q3 | 0.203125 | 0.162429 | 0.056146 | -0.103794 |

28.6.4. 시간 리샘플링 그룹화#

N = 15

times = pd.date_range("2017-05-20 00:00", freq="1min", periods=N)

df = pd.DataFrame({"time": times,

"value": np.arange(N)})

df

| time | value | |

|---|---|---|

| 0 | 2017-05-20 00:00:00 | 0 |

| 1 | 2017-05-20 00:01:00 | 1 |

| 2 | 2017-05-20 00:02:00 | 2 |

| 3 | 2017-05-20 00:03:00 | 3 |

| 4 | 2017-05-20 00:04:00 | 4 |

| 5 | 2017-05-20 00:05:00 | 5 |

| 6 | 2017-05-20 00:06:00 | 6 |

| 7 | 2017-05-20 00:07:00 | 7 |

| 8 | 2017-05-20 00:08:00 | 8 |

| 9 | 2017-05-20 00:09:00 | 9 |

| 10 | 2017-05-20 00:10:00 | 10 |

| 11 | 2017-05-20 00:11:00 | 11 |

| 12 | 2017-05-20 00:12:00 | 12 |

| 13 | 2017-05-20 00:13:00 | 13 |

| 14 | 2017-05-20 00:14:00 | 14 |

df.set_index("time").resample("5min").count()

| value | |

|---|---|

| time | |

| 2017-05-20 00:00:00 | 5 |

| 2017-05-20 00:05:00 | 5 |

| 2017-05-20 00:10:00 | 5 |

df2 = pd.DataFrame({"time": times.repeat(3),

"key": np.tile(["a", "b", "c"], N),

"value": np.arange(N * 3.)})

df2.head(7)

| time | key | value | |

|---|---|---|---|

| 0 | 2017-05-20 00:00:00 | a | 0.0 |

| 1 | 2017-05-20 00:00:00 | b | 1.0 |

| 2 | 2017-05-20 00:00:00 | c | 2.0 |

| 3 | 2017-05-20 00:01:00 | a | 3.0 |

| 4 | 2017-05-20 00:01:00 | b | 4.0 |

| 5 | 2017-05-20 00:01:00 | c | 5.0 |

| 6 | 2017-05-20 00:02:00 | a | 6.0 |

time_key = pd.Grouper(freq="5min")

resampled = (df2.set_index("time")

.groupby(["key", time_key])

.sum())

resampled

| value | ||

|---|---|---|

| key | time | |

| a | 2017-05-20 00:00:00 | 30.0 |

| 2017-05-20 00:05:00 | 105.0 | |

| 2017-05-20 00:10:00 | 180.0 | |

| b | 2017-05-20 00:00:00 | 35.0 |

| 2017-05-20 00:05:00 | 110.0 | |

| 2017-05-20 00:10:00 | 185.0 | |

| c | 2017-05-20 00:00:00 | 40.0 |

| 2017-05-20 00:05:00 | 115.0 | |

| 2017-05-20 00:10:00 | 190.0 |

resampled.reset_index()

| key | time | value | |

|---|---|---|---|

| 0 | a | 2017-05-20 00:00:00 | 30.0 |

| 1 | a | 2017-05-20 00:05:00 | 105.0 |

| 2 | a | 2017-05-20 00:10:00 | 180.0 |

| 3 | b | 2017-05-20 00:00:00 | 35.0 |

| 4 | b | 2017-05-20 00:05:00 | 110.0 |

| 5 | b | 2017-05-20 00:10:00 | 185.0 |

| 6 | c | 2017-05-20 00:00:00 | 40.0 |

| 7 | c | 2017-05-20 00:05:00 | 115.0 |

| 8 | c | 2017-05-20 00:10:00 | 190.0 |

28.7. 윈도우 함수 활용#

base_url = "https://raw.githubusercontent.com/codingalzi/datapy/master/jupyter-book/examples/"

file = "stock_px.csv"

close_px_all = pd.read_csv(base_url+file, parse_dates=True, index_col=0)

close_px = close_px_all[["AAPL", "MSFT", "XOM"]]

close_px = close_px.resample("B").ffill()

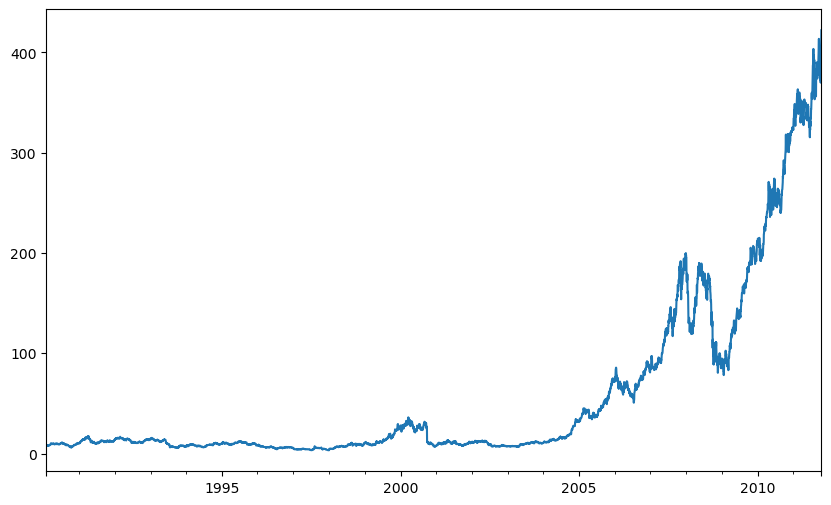

close_px["AAPL"].plot()

<Axes: >

#! figure,id=apple_daily_ma250,title="Apple price with 250-day moving average"

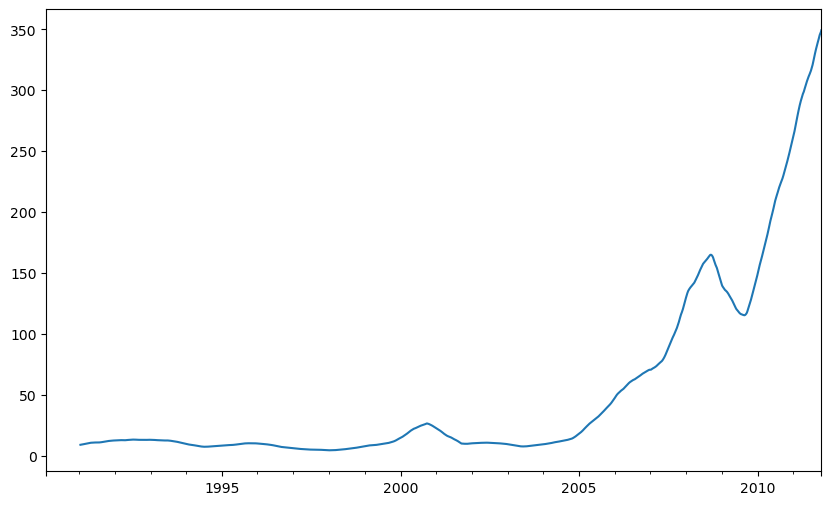

close_px["AAPL"].rolling(250).mean().plot()

<Axes: >

plt.figure()

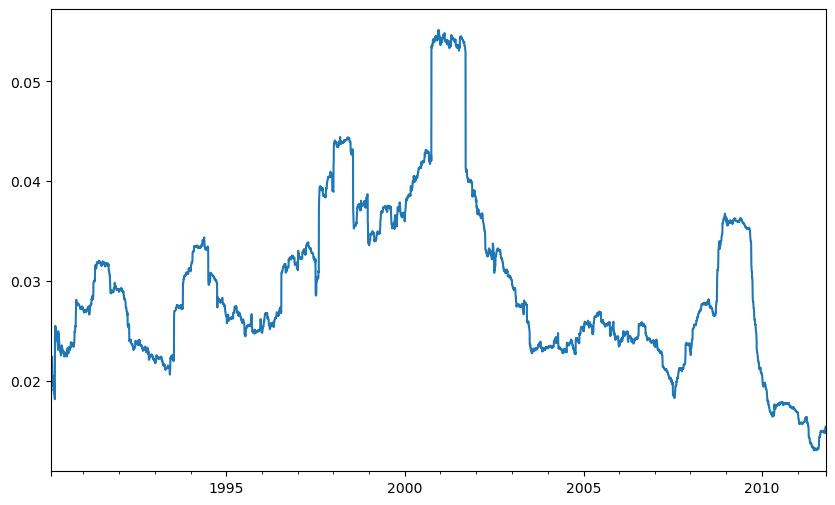

std250 = close_px["AAPL"].pct_change().rolling(250, min_periods=10).std()

std250[5:12]

#! figure,id=apple_daily_std250,title="Apple 250-day daily return standard deviation"

std250.plot()

<Axes: >

expanding_mean = std250.expanding().mean()

plt.figure()

plt.style.use('grayscale')

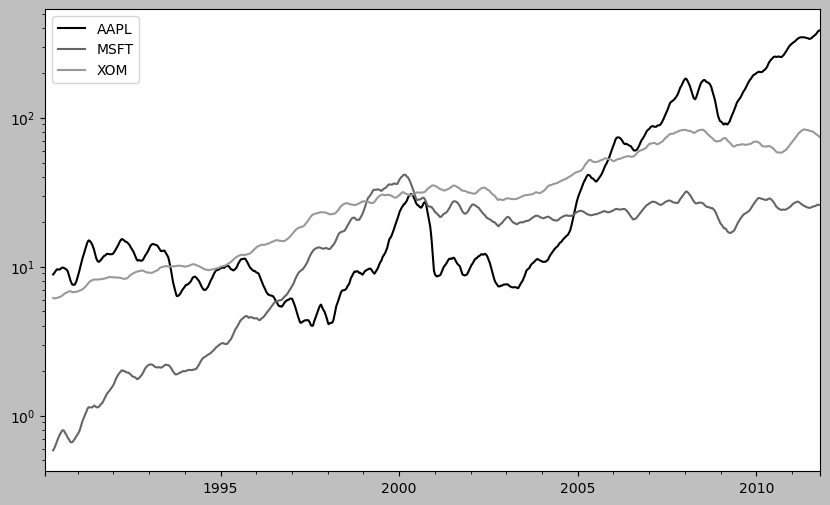

#! figure,id=stocks_daily_ma60,title="Stock prices 60-day moving average (log y-axis)"

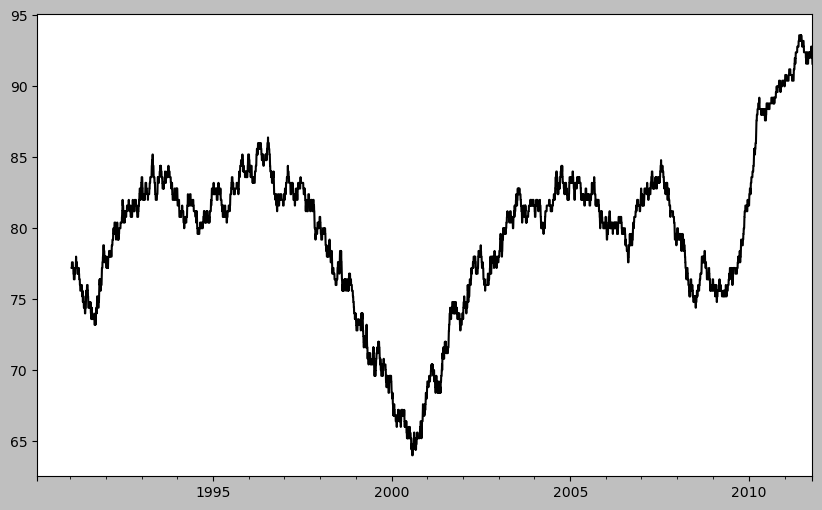

close_px.rolling(60).mean().plot(logy=True)

<Axes: >

<Figure size 1000x600 with 0 Axes>

close_px.rolling("20D").mean()

| AAPL | MSFT | XOM | |

|---|---|---|---|

| 1990-02-01 | 7.860000 | 0.510000 | 6.120000 |

| 1990-02-02 | 7.930000 | 0.510000 | 6.180000 |

| 1990-02-05 | 8.013333 | 0.510000 | 6.203333 |

| 1990-02-06 | 8.040000 | 0.510000 | 6.210000 |

| 1990-02-07 | 7.986000 | 0.510000 | 6.234000 |

| ... | ... | ... | ... |

| 2011-10-10 | 389.351429 | 25.602143 | 72.527857 |

| 2011-10-11 | 388.505000 | 25.674286 | 72.835000 |

| 2011-10-12 | 388.531429 | 25.810000 | 73.400714 |

| 2011-10-13 | 388.826429 | 25.961429 | 73.905000 |

| 2011-10-14 | 391.038000 | 26.048667 | 74.185333 |

5662 rows × 3 columns

28.7.1. 지수 가중치 함수#

plt.figure()

aapl_px = close_px["AAPL"]["2006":"2007"]

ma30 = aapl_px.rolling(30, min_periods=20).mean()

ewma30 = aapl_px.ewm(span=30).mean()

aapl_px.plot(style="k-", label="Price")

ma30.plot(style="k--", label="Simple Moving Avg")

ewma30.plot(style="k-", label="EW MA")

#! figure,id=timeseries_ewma,title="Simple moving average versus exponentially weighted"

plt.legend()

<matplotlib.legend.Legend at 0x255a3259000>

28.7.2. 이진 이동 윈도우 함수#

plt.figure()

spx_px = close_px_all["SPX"]

spx_rets = spx_px.pct_change()

returns = close_px.pct_change()

corr = returns["AAPL"].rolling(125, min_periods=100).corr(spx_rets)

#! figure,id=roll_correl_aapl,title="Six-month AAPL return correlation to S&P 500"

corr.plot()

<Axes: >

plt.figure()

corr = returns.rolling(125, min_periods=100).corr(spx_rets)

#! figure,id=roll_correl_all,title="Six-month return correlations to S&P 500"

corr.plot()

<Axes: >

<Figure size 1000x600 with 0 Axes>

28.7.3. 사용자 정의 윈도우 함수#

plt.figure()

from scipy.stats import percentileofscore

def score_at_2percent(x):

return percentileofscore(x, 0.02)

result = returns["AAPL"].rolling(250).apply(score_at_2percent)

#! figure,id=roll_apply_ex,title="Percentile rank of 2% AAPL return over one-year window"

result.plot()

<Axes: >